The Missing Control Plane for Agentic Payments

May 5, 2026Stablecoins make money programmable for agents. RTP/RfP and FedNow make U.S. dollars available instantly. AppBrilliance makes the funding event usable, authorized, and commercially viable.

Strategic Framing

Bradley Riss, Co-CEO of AppBrilliance, is right in the thesis he shared: agents will need payment systems that are instant, programmable, low-cost at small transaction sizes, and final.

The low-cost point matters. Many card-based agentic payment schemes inherit card economics: per-transaction fees of $0.25 + 2.9% or more in many cases. Those economics are difficult to reconcile with agents making frequent, small, delegated payments, especially where the agent may need to initiate multiple transactions as part of a single task.

Stablecoins can enable the low-cost, programmable transactions agentic payments require, but if the stablecoin account or wallet is funded through existing card rails, the system imports chargeback risk and much of the same cost structure it was supposed to avoid. The unresolved first-mile question remains: how does the user fund the account or wallet with U.S. dollars in the first place?

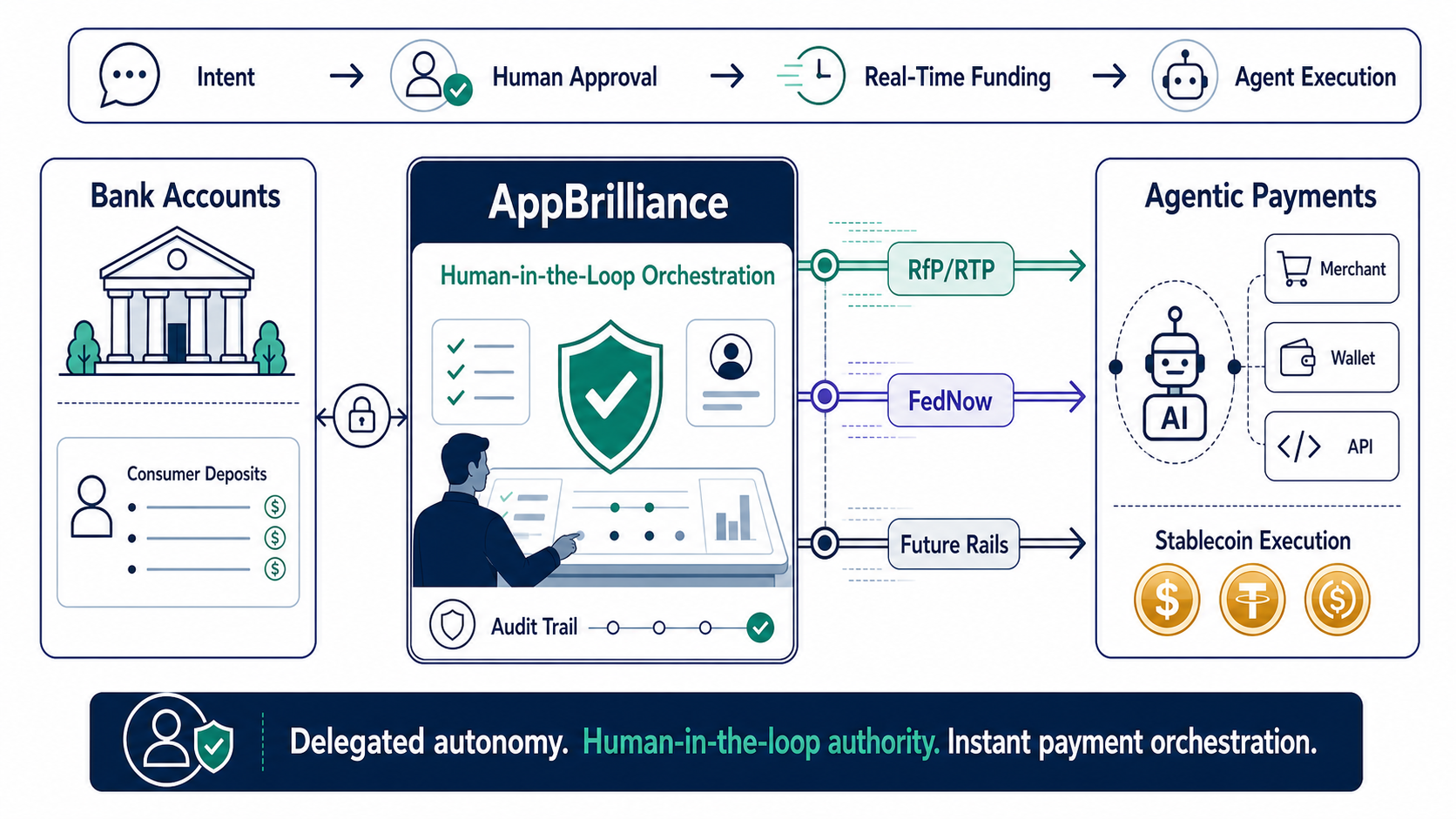

The scarce layer in agentic payments will be trusted, human-authorized movement from bank accounts into programmable execution environments.

In other words, the agentic payments stack is splitting into three layers:

- Intent and authorization: What did the human authorize the agent to do?

- Funding: How does real money move from the user’s bank account into an agent-controlled or agent-accessible execution environment?

- Execution: How does the agent spend against APIs, merchants, digital services, stablecoin rails, or closed-loop environments?

The industry is moving quickly on layers 1 and 3. Google AP2, OpenAI/Stripe ACP, Visa Trusted Agent Protocol, Mastercard Agent Pay, Coinbase x402, and Cloudflare NET Dollar all validate that agentic commerce is becoming a real category.

AppBrilliance’s wedge is layer 2: human-in-the-loop real-time funding over bank rails.

That is a more valuable position than it first appears, because every agentic system eventually runs into the same bottleneck: value still begins in bank accounts.

What the Industry Is Signaling

The leading payments and AI platforms are racing to define who controls the trust layer.

OpenAI and Stripe’s Agentic Commerce Protocol positions ChatGPT as a shopping agent that can pass order and payment details to merchants while keeping the merchant of record intact. OpenAI emphasizes that users explicitly confirm steps, tokens are scoped to specific merchants and amounts, and merchants keep their existing payment systems and customer relationships.

Google’s AP2 takes a broader protocol view. It frames the core problem as authorization, authenticity, and accountability when an agent initiates a payment instead of a human directly clicking buy. Its answer is a chain of signed mandates: intent, cart, and payment evidence. Importantly, Google says AP2 is payment-method agnostic and supports cards, stablecoins, and real-time bank transfers.

Visa’s Trusted Agent Protocol attacks the merchant-recognition problem. Its claim is that merchants need to distinguish trusted buying agents from bots, preserve visibility into the consumer, and receive agent intent and payment information through cryptographic signatures.

Mastercard Agent Pay attacks the credential-control problem from the card-network side. Mastercard’s Agentic Tokens are designed to let agents transact with trusted, tokenized credentials while consumers retain control over what an agent is allowed to purchase.

Coinbase x402 and Cloudflare NET Dollar attack the internet-native execution problem. x402 turns HTTP’s dormant “payment required” concept into a stablecoin-based payment flow for APIs, apps, and AI agents. Cloudflare’s NET Dollar announcement frames stablecoins as infrastructure for pay-per-use, fractional payments, and microtransactions across the agentic web.

Visa’s stablecoin settlement program shows that stablecoins are moving out of crypto ideology and into payments operations. As of April 29, 2026, Visa said its stablecoin settlement pilot had reached a $7 billion annualized run rate and expanded to nine blockchains.

Taken together, the industry is saying five things:

- Agentic commerce is real enough that incumbents are building protocols, tokens, and network rules.

- User authorization and auditability are central, not secondary.

- Stablecoins are becoming a serious execution and settlement layer.

- Existing payment networks want agents to stay inside their credential and risk frameworks.

- No one has fully solved the first-mile bank-account funding experience for agentic wallets and real-time account-to-account payments.

That last point is where the AppBrilliance platform provides a solution.

The Strategic Gap: Everyone Wants Agent Spending, but Someone Has to Fund the Agent

The common agentic payment narratives start at checkout:

- The agent finds the product.

- The merchant validates the agent.

- The agent presents a token or mandate.

- The merchant accepts payment.

That is incomplete.

If the agent is paying with a card credential, the issuer and network control the payment. If it is paying with a stablecoin, the wallet needs to already be funded. If it is paying out of a closed-loop wallet, the wallet balance has to exist. If it is paying an API through x402, the client needs spendable stablecoin value.

So the strategic question becomes:

For most U.S. consumers and businesses, the answer is still a bank account. Payroll lands there. Operating cash sits there. Treasury controls are there. FDIC-insured deposits are there. For all the excitement around stablecoins, the bank account remains the source of funds for mainstream adoption.

That makes real-time bank funding the bridge between the old money system and the new agentic execution layer.

AppBrilliance provides that bridge.

Why Human-in-the-Loop Is a Feature, Not a Compromise

The phrase “human-in-the-loop” can sound like a limitation in an AI market obsessed with autonomy. In payments, it is the opposite. It is the trust anchor.

The unlock for Agentic payments is not free-spending Agents. It’s Agents that can spend within the boundaries that we authorize.

People should not approve every microtransaction. That kills the agentic value proposition. But people should define and approve the mandate, supervise the funding event, control the wallet threshold, approve the merchant category, and monitor the spending cap.

Google’s AP2 separates real-time purchases from delegated tasks and uses mandates to prove what the user authorized. Mastercard emphasizes consumer control over what the agent can purchase. OpenAI says early agentic checkout should keep users explicitly confirming steps. Visa frames trusted-agent commerce around agent identity, consumer recognition, and payment data.

That’s trust. Even more importantly, to fund these Agentic wallets, the human must be in the loop to operate a real-time good-funds rail provided by their bank.

AppBrilliance extends that industry consensus into the bank-account funding layer:

The agent may initiate the need for funds. The user authorizes and supervises the movement of funds. The bank executes the movement of funds. The wallet or merchant receives instant good funds from the bank transfer.

This is the architecture that makes agentic payments commercially viable.

Why RTP/RfP and FedNow Matter Strategically

Stablecoins are excellent for low-cost programmable execution, but they do not automatically solve fiat funding, consumer authorization, or bank-account trust.

That distinction is critical: a low-cost stablecoin transaction is only truly low cost if the funding path does not rely on expensive, reversible card rails.

RTP/RfP and FedNow solve a different problem:

- They move bank money in real time.

- They provide immediate availability of funds.

- They support 24/7/365 operation.

- They are built around finality rather than chargeback logic.

- They support ISO 20022 messaging and richer payment context.

- Requests for Payment require payer consent before funds are pushed.

This matters because the agentic wallet funding event has three requirements:

- Speed: The agent cannot wait days.

- Certainty: The downstream wallet or merchant needs good funds.

- Control: The human must approve sensitive money movement.

Cards solve broad acceptance but bring interchange, reversibility, and card-network economics. ACH solves low cost but brings delayed returns, NSF risk, and settlement uncertainty. Wires solve finality but not consumer usability or micro/frequent funding economics. RTP/FedNow are the first U.S. bank rails that plausibly satisfy the funding event.

AppBrilliance’s Value Thesis

AppBrilliance is an orchestration layer for human-authorized real-time money movement, not another data aggregation provider. Think write-enabled Open Banking for payments.

1. AppBrilliance owns the first-mile funding problem

Stablecoin systems, agentic checkout protocols, and closed-loop wallets all need funded balances or payment credentials. AppBrilliance sits where value moves from bank account to execution environment.

That funding moment is high-friction today. The user’s journey can involve merchant checkout, bank selection, authentication, request discovery, payment approval, status uncertainty, and return to merchant. AppBrilliance’s agentic flow compresses that workflow into an embedded, guided experience while keeping the user present in the banking flow for compliance, authentication, and authorization.

2. AppBrilliance turns bank UIs and bank rails into agent-compatible infrastructure

Open banking in the U.S. is mostly about data access, not payment execution. Banks do not expose payment-initiation APIs to third parties. AppBrilliance’s distinctive approach is to orchestrate payment workflows through existing user-attended and authenticated bank surfaces like online banking to interact with real-time rails.

That is strategically different from data aggregation, credential vaulting, or a pure API gateway. The core value is workflow execution inside the real constraints of U.S. banking.

3. AppBrilliance provides instant good funds without card economics

For merchants, wallets, gaming operators, marketplaces, billers, and other high-frequency funding use cases, the pitch is not only “cheaper than cards,” it is:

- Fewer payment failures

- Less abandonment from fragmented RfP flows

- Instant confirmation

- No card chargeback model

- Lower acceptance cost

- Better fit for wallet reloads and account-to-account funding

Agentic commerce makes this more important because agents will increase transaction frequency and expose the weakness of payment methods built for occasional human checkout.

4. AppBrilliance is an authorization layer, not just a payment layer

In agentic payments, the most valuable metadata may be the evidence of authorization: who approved, for what purpose, under what constraints, at what time, from which account, into which wallet or merchant, and with what result.

That positions AppBrilliance to solve the specific funding problem that protocols and mandates alone do not.